Wednesday, April 30, 2008

Fed Cuts don't necessarily lower mortgage rates

I thought it would be a good idea to post a link to my previous post which explains why Fed Rate cuts DO NOT lower mortgage rates. Here is a link to the article.

Rate Update April 30, 2008

The markets are eagerly awaiting the Fed’s announcement which is scheduled to be announced at 2:15PM EST. Analysts expect that the Fed will cut short term rates by an additional .25%. As we’ve mentioned throughout this rate cutting cycle the Fed’s rate cut in and of itself will not move the markets. What could drive the markets is the tone of the Fed’s statement following the announcement. Here is a summary of what to listen for:

*If the Fed stresses concern about inflation in their statement over economic recovery it is likely a sign that the Fed is done cutting rates in the near-term. Although concern over inflation is bad for mortgage rates because the Fed is indicating that that they’ll pause it could actually strengthen the US Dollar and help mortgage rates.

*If the Fed maintains the view that their concern for inflation is “balanced” with economic growth then they are likely leaving the door open for future Fed cuts. In this instance we do not believe mortgage rates would benefit because of inflationary pressures.

To give you an idea of the scrutiny that the Fed faces in crafting their language for their statement you may want to check out this article from Marketwatch. Maybe they should begin hiring English Majors instead of Economists for this task…..

Current Outlook: neutral

*If the Fed stresses concern about inflation in their statement over economic recovery it is likely a sign that the Fed is done cutting rates in the near-term. Although concern over inflation is bad for mortgage rates because the Fed is indicating that that they’ll pause it could actually strengthen the US Dollar and help mortgage rates.

*If the Fed maintains the view that their concern for inflation is “balanced” with economic growth then they are likely leaving the door open for future Fed cuts. In this instance we do not believe mortgage rates would benefit because of inflationary pressures.

To give you an idea of the scrutiny that the Fed faces in crafting their language for their statement you may want to check out this article from Marketwatch. Maybe they should begin hiring English Majors instead of Economists for this task…..

Current Outlook: neutral

Tuesday, April 29, 2008

Rate Update April 29, 2008

Mortgage-backed bonds are trading modestly higher this morning pushing 30 year rates slightly lower. Watch today’s you tube video to understand what we’ll be listening for in tomorrow’s Fed announcement.

From a technical standpoint mortgage-backed bonds are trading against a ceiling of resistance. This means that all else being equal we’d expect prices to fall (pushing rates higher in the next couple days). A strong Fed statement indicating that they feel inflation pressures will curb in the coming months could help us break this resistance pushing rates lower.

Current Outlook: neutral with locking bias

Monday, April 28, 2008

The Four "C"s of qualifying for a mortgage

In evaluating a loan application to determine wether or not an applicant qualifies for a mortgage lenders look at four areas. These four areas are known as the "Four C's" and stand for:

1) Credit

2) Capacity

3) Capital

4) Collateral

Here is a summary of each "C" and how they impact the loan approval process:

Credit:

Credit is arguably the most important factor of the 4 C’s. An applicant’s credit score taken from the credit report is the simplest measure of their credit strength. In determining an applicant’s credit score lenders will simply use the middle of the three credit scores reported by the three credit repositories (Transunion, Equifax, & Experian).

Credit scores are heavily influenced by a person’s payment history over the preceding 24 months. Other factors may include the proportion of revolving debt relative to the high credit limits, number of accounts, lack of credit depth, and many more.

Another factor that lenders may pay attention to in an applicant’s credit profile is their housing payment history over the preceding 12 months. This may be reflective in a previous mortgage on the credit report or by verifying rent payments if the applicant does not currently own a home.

Finally, bankruptcies, judgments, and foreclosures can all negatively impact the credit analysis for an applicant. Just because an applicant has these negative marks on their credit report doesn’t mean they cannot get approved for a mortgage. It simply means that they would have to show other compensating factors and/ or may have to accept higher rates and terms.

Capacity:

In addition to reviewing an applicant’s credit banks want to analyze their ability to repay the mortgage over time. The primary tool they use for this analysis is a debt-to-income ratio. Simply put, the debt-to-income ratio is the sum of all monthly payment obligations an applicant has (including the proposed housing payment) divided by their gross monthly income.

For example, here is a hypothetical debt-to-income calculation for John & Jane Doe

Obligations:

*Proposed housing payment (including real estate taxes and homeowner’s insurance): $2,000

*Car payments: $250

*Student loans: $150

*Minimum monthly payments on credit cards: $75

Income:

John’s monthly gross income: $5,000

Jane’s monthly gross income: $5,000

Debt-to-income calculation:

Total obligations: $2,000+$250+$150+$75= $2,475

Total income: $5,000+$5,000= $10,000

DTI=24.75%

In this case the debt-to-income ratio of 24.75% would likely be viewed upon favorably by the lender. In most cases banks will accept DTI’s as high as 45% and in some cases up to 50-65%.

Capital:

Does an applicant have a financial cushion to fall back on if their income is unexpectedly interrupted for a period of time? Has the applicant shown a pattern and habit of saving money over time? These are important questions to a lender and can be answered by reviewing an applicant’s capital accounts.

Capital accounts are any account with liquid assets that a borrower could access if need be. The most common forms of capital accounts on a loan application are checking, savings, money market, brokerage, IRA, and 401K accounts.

In most cases the bank will want to verify that an applicant has an amount equal to 2 months worth of their total housing payment (including real estate taxes and homeowner’s insurance) saved up in a capital account after they subtract any cash required for down-payment & settlement charges. If the mortgage is going to be secured by an investment property or second home the bank may want to see more capital for the applicant.

There are loan programs and lenders that do not require any capital or will allow capital to be gifted from family members.

Collateral:

The final piece of the mortgage application that the bank is interested in reviewing is the property itself. After all, if a borrower fails to make their monthly payments then the bank will take the house back and sell it in order to recoup the money that they loaned against it.

The value of a home will generally be determined by a professional appraiser’s appraisal report. Although, over the past few years automated and data base driven appraisals have become more common.

In reviewing the collateral for a property the bank will review two basic questions:

a) Does the appraiser’s determination of value for the subject property support the value that the applicant is buying (or refinancing) it for?

There are multiple methodologies for determining the value of a home. The two that show up in an appraisal report are the “cost approach” and the “sales comparison approach”.

The “cost approach” determines the value of a home based on the value to rebuild or replicate the property from scratch. This analysis will take into consideration the value of the land that the home is built on and add the cost to rebuild the improvements based on the square footage and amenities (i.e. basements, garages, etc.). The “cost approach” is less relevant to a bank because they never intend on rebuilding the property. However, they may review this in determining if the homeowner’s insurance policy provides enough coverage.

The “sales analysis approach” is the most relevant to lenders in determining the value of the collateral property. With this approach an appraiser will find what they consider to be the 3-6 most comparable properties that have sold near (usually within 1 mile) the subject property within the past 12 months.

The appraiser will then make adjustments to the value of the subject property by comparing various features of the home. Among the factors that can impact the adjustments are square footage, view, quality of construction, built in amenities/ upgrades, number of bedroom and bathrooms, heating cooling systems, etc.

The value as determined by the sales analysis approach is the most important in determining the value for the home in the lender’s perspective.

b) What is the ratio of the loan amount to the value of the property (LTV)?

The loan-to-value (LTV) ratio is also an important consideration for the bank. The LTV measures the amount of money the lender is lending against the value of the collateral.

All else being equal a greater LTV is riskier for the bank than the same loan application with a lower LTV. This is because in the event of foreclosure it is less probable that the lender will recoup the entire loan versus a loan with a higher LTV.

Important Thresholds

There are important thresholds in the underwriting guidelines of most banks which make it more or less likely that a loan will get approved or that a loan will be approved with more favorable or less favorable terms.

These are:

-LTV=

<70%- with an LTV of less than 70% the lender will generally feel very comfortable with the loan. This is because the borrower has a significant of “skin in the game” such that if they should fall behind on their payments they will likely do whatever they can to pay the loan current before foreclosures sets in. Lenders know this and therefore are less concerned about the other 3 C’s with these applications.

70-80%- In general lenders are also very comfortable with an LTV between 70% & 80%. This is because they know that if they had to foreclose on a property it is likely that they could recoup the loan with little risk.

80.01-90%- At 80-90% LTVs bank begin to look for other compensating factors in the file. They may begin looking closer at an applicant’s reserves, income, or source of down payment. It is likely that the bank may charge a premium to the interest rate of anywhere from 0%-.50% depending on the loan file.

Furthermore, if the applicant elects to do 1 loan they will require some form of mortgage insurance. Mortgage insurance is an insurance policy that the borrower usually pays for. The insurance would cover a portion of the lenders losses in the event that they had to foreclose on the property and they did not recoup the entire loan.

90.01%-95%- With less and less equity in the transaction a lender will certainly want to see other compensating factors at higher LTVs. This would include higher credit scores, greater reserves, employment stability, etc. The lender may impose a risk premium to the interest rate of .125%-1.00% Again, with one loan the lender will require the borrower purchase mortgage insurance in the event that they default on their payments.

95.01%-100%- With less than 5% equity into the transaction the lender will make sure that the borrower has ample reserves and solid credit. At these levels the lender is at the most amount of risk because in the event that the borrower defaults and forecloses on the home in the initial couple years it is almost guaranteed that the lender will incur a loss. Borrowers will typically pay a .25%-2.00% premium to their interest rate for this type of approach.

1) Credit

2) Capacity

3) Capital

4) Collateral

Here is a summary of each "C" and how they impact the loan approval process:

Credit:

Credit is arguably the most important factor of the 4 C’s. An applicant’s credit score taken from the credit report is the simplest measure of their credit strength. In determining an applicant’s credit score lenders will simply use the middle of the three credit scores reported by the three credit repositories (Transunion, Equifax, & Experian).

Credit scores are heavily influenced by a person’s payment history over the preceding 24 months. Other factors may include the proportion of revolving debt relative to the high credit limits, number of accounts, lack of credit depth, and many more.

Another factor that lenders may pay attention to in an applicant’s credit profile is their housing payment history over the preceding 12 months. This may be reflective in a previous mortgage on the credit report or by verifying rent payments if the applicant does not currently own a home.

Finally, bankruptcies, judgments, and foreclosures can all negatively impact the credit analysis for an applicant. Just because an applicant has these negative marks on their credit report doesn’t mean they cannot get approved for a mortgage. It simply means that they would have to show other compensating factors and/ or may have to accept higher rates and terms.

Capacity:

In addition to reviewing an applicant’s credit banks want to analyze their ability to repay the mortgage over time. The primary tool they use for this analysis is a debt-to-income ratio. Simply put, the debt-to-income ratio is the sum of all monthly payment obligations an applicant has (including the proposed housing payment) divided by their gross monthly income.

For example, here is a hypothetical debt-to-income calculation for John & Jane Doe

Obligations:

*Proposed housing payment (including real estate taxes and homeowner’s insurance): $2,000

*Car payments: $250

*Student loans: $150

*Minimum monthly payments on credit cards: $75

Income:

John’s monthly gross income: $5,000

Jane’s monthly gross income: $5,000

Debt-to-income calculation:

Total obligations: $2,000+$250+$150+$75= $2,475

Total income: $5,000+$5,000= $10,000

DTI=24.75%

In this case the debt-to-income ratio of 24.75% would likely be viewed upon favorably by the lender. In most cases banks will accept DTI’s as high as 45% and in some cases up to 50-65%.

Capital:

Does an applicant have a financial cushion to fall back on if their income is unexpectedly interrupted for a period of time? Has the applicant shown a pattern and habit of saving money over time? These are important questions to a lender and can be answered by reviewing an applicant’s capital accounts.

Capital accounts are any account with liquid assets that a borrower could access if need be. The most common forms of capital accounts on a loan application are checking, savings, money market, brokerage, IRA, and 401K accounts.

In most cases the bank will want to verify that an applicant has an amount equal to 2 months worth of their total housing payment (including real estate taxes and homeowner’s insurance) saved up in a capital account after they subtract any cash required for down-payment & settlement charges. If the mortgage is going to be secured by an investment property or second home the bank may want to see more capital for the applicant.

There are loan programs and lenders that do not require any capital or will allow capital to be gifted from family members.

Collateral:

The final piece of the mortgage application that the bank is interested in reviewing is the property itself. After all, if a borrower fails to make their monthly payments then the bank will take the house back and sell it in order to recoup the money that they loaned against it.

The value of a home will generally be determined by a professional appraiser’s appraisal report. Although, over the past few years automated and data base driven appraisals have become more common.

In reviewing the collateral for a property the bank will review two basic questions:

a) Does the appraiser’s determination of value for the subject property support the value that the applicant is buying (or refinancing) it for?

There are multiple methodologies for determining the value of a home. The two that show up in an appraisal report are the “cost approach” and the “sales comparison approach”.

The “cost approach” determines the value of a home based on the value to rebuild or replicate the property from scratch. This analysis will take into consideration the value of the land that the home is built on and add the cost to rebuild the improvements based on the square footage and amenities (i.e. basements, garages, etc.). The “cost approach” is less relevant to a bank because they never intend on rebuilding the property. However, they may review this in determining if the homeowner’s insurance policy provides enough coverage.

The “sales analysis approach” is the most relevant to lenders in determining the value of the collateral property. With this approach an appraiser will find what they consider to be the 3-6 most comparable properties that have sold near (usually within 1 mile) the subject property within the past 12 months.

The appraiser will then make adjustments to the value of the subject property by comparing various features of the home. Among the factors that can impact the adjustments are square footage, view, quality of construction, built in amenities/ upgrades, number of bedroom and bathrooms, heating cooling systems, etc.

The value as determined by the sales analysis approach is the most important in determining the value for the home in the lender’s perspective.

b) What is the ratio of the loan amount to the value of the property (LTV)?

The loan-to-value (LTV) ratio is also an important consideration for the bank. The LTV measures the amount of money the lender is lending against the value of the collateral.

All else being equal a greater LTV is riskier for the bank than the same loan application with a lower LTV. This is because in the event of foreclosure it is less probable that the lender will recoup the entire loan versus a loan with a higher LTV.

Important Thresholds

There are important thresholds in the underwriting guidelines of most banks which make it more or less likely that a loan will get approved or that a loan will be approved with more favorable or less favorable terms.

These are:

-LTV=

<70%- with an LTV of less than 70% the lender will generally feel very comfortable with the loan. This is because the borrower has a significant of “skin in the game” such that if they should fall behind on their payments they will likely do whatever they can to pay the loan current before foreclosures sets in. Lenders know this and therefore are less concerned about the other 3 C’s with these applications.

70-80%- In general lenders are also very comfortable with an LTV between 70% & 80%. This is because they know that if they had to foreclose on a property it is likely that they could recoup the loan with little risk.

80.01-90%- At 80-90% LTVs bank begin to look for other compensating factors in the file. They may begin looking closer at an applicant’s reserves, income, or source of down payment. It is likely that the bank may charge a premium to the interest rate of anywhere from 0%-.50% depending on the loan file.

Furthermore, if the applicant elects to do 1 loan they will require some form of mortgage insurance. Mortgage insurance is an insurance policy that the borrower usually pays for. The insurance would cover a portion of the lenders losses in the event that they had to foreclose on the property and they did not recoup the entire loan.

90.01%-95%- With less and less equity in the transaction a lender will certainly want to see other compensating factors at higher LTVs. This would include higher credit scores, greater reserves, employment stability, etc. The lender may impose a risk premium to the interest rate of .125%-1.00% Again, with one loan the lender will require the borrower purchase mortgage insurance in the event that they default on their payments.

95.01%-100%- With less than 5% equity into the transaction the lender will make sure that the borrower has ample reserves and solid credit. At these levels the lender is at the most amount of risk because in the event that the borrower defaults and forecloses on the home in the initial couple years it is almost guaranteed that the lender will incur a loss. Borrowers will typically pay a .25%-2.00% premium to their interest rate for this type of approach.

Rate Update April 28, 2008

We don’t expect a lot of volatility until tomorrow afternoon when traders begin to position their portfolios ahead of an action-packed Wednesday, Thursday, & Friday. Watch today’s you tube video to find out what is on the schedule that could impact mortgage rates this week.

Current Outlook: neutral

Friday, April 18, 2008

Rate Update April 18, 2008

Mortgage rates continue to increase thanks to momentum in the stock market. Mortgage rates have increase .25%-.50% across the board this week because of better than expected earnings reports. We’ve explained in the past on ‘rate update’ that mortgage rates often suffer from a rally in the stock market because fund managers have to sell bonds in order to create capital to buy into the stock market.

Today better than expected results out of Google & Citi Group are the culprits.

Current Outlook: locking

Today better than expected results out of Google & Citi Group are the culprits.

Current Outlook: locking

Thursday, April 17, 2008

Rate Update April 17, 2008

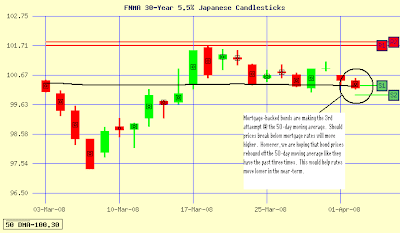

We thought that bond prices may hold at the 50-day moving average yesterday as they had the last four times that they tested this level. However, the stock market rally was too strong which pushed rates higher again. Here is a chart which shows pricing dropping below the 50-day moving average (black line):

From a technical perspective mortgage-backed bonds still have some room to drift lower so we might see rates move higher by another .125%-.25% before they stabilize. What could save the day? Merrill lynch reported weaker than expected earnings earlier today and Citi Bank is scheduled to release their earnings report tomorrow. Another weak report could help mortgage-backed bonds rebound and hopefully push rates lower.

Current Outlook: locking

From a technical perspective mortgage-backed bonds still have some room to drift lower so we might see rates move higher by another .125%-.25% before they stabilize. What could save the day? Merrill lynch reported weaker than expected earnings earlier today and Citi Bank is scheduled to release their earnings report tomorrow. Another weak report could help mortgage-backed bonds rebound and hopefully push rates lower.

Current Outlook: locking

Wednesday, April 16, 2008

Article about debt snowball pay-off for consumer debt

In Praise of the Debt Snowball

Thursday, 28th September 2006 (by J.D.)

This article is about Choices, Credit Cards, Debt

During my twenties, I accumulated nearly $25,000 in consumer debt. I had a spending problem. With time, I was able to get my spending under control (mostly), but I still owned overwhelming debt. How could I get rid of it?

The personal finance books all suggested the same approach:

Order your debts from highest interest rate to lowest interest rate.

Designate a certain amount of money to pay toward debts each month.

Pay the minimum payment on all debts except the one with the highest interest rate.

Throw every other penny at the debt with the highest interest rate.

When that debt is gone, do not alter the monthly amount used to pay debts, but throw all you can at the debt with the next-highest interest rate.

This made perfect sense. By doing this, I would be paying the minimum amount in interest over the long term. The trouble was, my highest-interest rate debt was also my debt with the biggest balance (a fully-maxed $12,000 credit card at 19.8% interest). I’d plug away at this debt for several months at a time, but then give up because it felt like I was never getting anywhere.

This happened over and over. I’d start and fail. Start and fail.

Then I read about the Debt Snowball method in Dave Ramsey’s The Total Money Makeover. The Debt Snowball method is similar to the traditional approach except that instead of attacking high-interest rate debts first, you attack low-balance debts first. Why? Because you’ll get the psychological lift of pinging debts off in rapid succession. And if you’re like me, this makes all the difference. The Debt Snowball approach is:

Order your debts from lowest balance to highest balance.

Designate a certain amount of money to pay toward debts each month.

Pay the minimum payment on all debts except the one with the lowest balance.

Throw every other penny at the debt with the lowest balance.

When that debt is gone, do not alter the monthly amount used to pay debts, but throw all you can at the debt with the next-lowest balance.

When I read about the Debt Snowball method, I was skeptical. I knew it would cost me more in the long run, at least on paper. But I figured I had nothing to lose. I tried it. In four months I’d paid off most of my debts. I was shocked. I’d been trying and failing for years, and now I was able to make a huge dent in just months? It was all because I had changed my approach just slightly.

Humans are complex psychological creatures. They’re not adding machines. Many of us know what we ought to do but find it difficult to actually make the best choices. If we were adding machines, we wouldn’t accumulate $20,000 in consumer debt in the first place! It’s misguided to tell somebody so deep in debt that they must follow the repayment plan that minimizes interest payments. The important thing to do is to set up a system of positive reinforcement, and that’s exactly what the Debt Snowball method does.

Which method should you choose? Do what works for you. The first method can save you money in the long-run. But if you’ve tried it and failed, give the Debt Snowball method a shot. It might be the answer you’re searching for!

Thursday, 28th September 2006 (by J.D.)

This article is about Choices, Credit Cards, Debt

During my twenties, I accumulated nearly $25,000 in consumer debt. I had a spending problem. With time, I was able to get my spending under control (mostly), but I still owned overwhelming debt. How could I get rid of it?

The personal finance books all suggested the same approach:

Order your debts from highest interest rate to lowest interest rate.

Designate a certain amount of money to pay toward debts each month.

Pay the minimum payment on all debts except the one with the highest interest rate.

Throw every other penny at the debt with the highest interest rate.

When that debt is gone, do not alter the monthly amount used to pay debts, but throw all you can at the debt with the next-highest interest rate.

This made perfect sense. By doing this, I would be paying the minimum amount in interest over the long term. The trouble was, my highest-interest rate debt was also my debt with the biggest balance (a fully-maxed $12,000 credit card at 19.8% interest). I’d plug away at this debt for several months at a time, but then give up because it felt like I was never getting anywhere.

This happened over and over. I’d start and fail. Start and fail.

Then I read about the Debt Snowball method in Dave Ramsey’s The Total Money Makeover. The Debt Snowball method is similar to the traditional approach except that instead of attacking high-interest rate debts first, you attack low-balance debts first. Why? Because you’ll get the psychological lift of pinging debts off in rapid succession. And if you’re like me, this makes all the difference. The Debt Snowball approach is:

Order your debts from lowest balance to highest balance.

Designate a certain amount of money to pay toward debts each month.

Pay the minimum payment on all debts except the one with the lowest balance.

Throw every other penny at the debt with the lowest balance.

When that debt is gone, do not alter the monthly amount used to pay debts, but throw all you can at the debt with the next-lowest balance.

When I read about the Debt Snowball method, I was skeptical. I knew it would cost me more in the long run, at least on paper. But I figured I had nothing to lose. I tried it. In four months I’d paid off most of my debts. I was shocked. I’d been trying and failing for years, and now I was able to make a huge dent in just months? It was all because I had changed my approach just slightly.

Humans are complex psychological creatures. They’re not adding machines. Many of us know what we ought to do but find it difficult to actually make the best choices. If we were adding machines, we wouldn’t accumulate $20,000 in consumer debt in the first place! It’s misguided to tell somebody so deep in debt that they must follow the repayment plan that minimizes interest payments. The important thing to do is to set up a system of positive reinforcement, and that’s exactly what the Debt Snowball method does.

Which method should you choose? Do what works for you. The first method can save you money in the long-run. But if you’ve tried it and failed, give the Debt Snowball method a shot. It might be the answer you’re searching for!

Rate Update April 16, 2008

30 year fixed rates are higher again this morning. Watch today’s you tube video to understand why rates have been pushed higher.

We’re closely watching technical trading patterns again as mortgage-backed bonds trade up against the 50-day moving average price line.

Current outlook: Cautiously floating

Tuesday, April 15, 2008

Rate Update April 15, 2008

Rates are slightly higher across the board this morning. Two things are working against mortgage rates.

First, as I mentioned in yesterday’s ‘rate update’ video we are in the heart of earnings season and a rally in the stock market could put upward pressure on mortgage rates. This is what is happening this morning after Johnson & Johnson (JNJ) reported better than expected first quarter earnings.

Second, the Producer Price Index (PPI), which reports on inflation at the wholesale/ manufacturing level of our economy, increased by over 1% in March. We know that inflation is the number one enemy of mortgage rates.

The good news is that mortgage backed-bonds are close to hitting tough technical trading support & the PPI report showed modest increases when you strip out volatile food and energy prices. We hope that traders will focus on these items as the day wears on. If not, we could see rates rise by another .25% before they stabilize.

Current Outlook: neutral

First, as I mentioned in yesterday’s ‘rate update’ video we are in the heart of earnings season and a rally in the stock market could put upward pressure on mortgage rates. This is what is happening this morning after Johnson & Johnson (JNJ) reported better than expected first quarter earnings.

Second, the Producer Price Index (PPI), which reports on inflation at the wholesale/ manufacturing level of our economy, increased by over 1% in March. We know that inflation is the number one enemy of mortgage rates.

The good news is that mortgage backed-bonds are close to hitting tough technical trading support & the PPI report showed modest increases when you strip out volatile food and energy prices. We hope that traders will focus on these items as the day wears on. If not, we could see rates rise by another .25% before they stabilize.

Current Outlook: neutral

Monday, April 14, 2008

Rate Update April 14, 2008

It will be a busy week for economic data to be released.

This morning we started the week off with the government releasing the monthly retail sales report. The report showed that retail sales in March were higher than what analysts had expected. Furthermore, the report revised February’s retail sales figure higher. Ordinarily this would pressure mortgage rates higher but analysts have shrugged their shoulders likely because they view this months report as an outlying figure in an overall weak trend.

Watch today’s you tube video to find what other reports and financial news will likely impact mortgage rates this week.

Current Outlook: neutral

Saturday, April 12, 2008

WSJ.com article points out importance of 30 yr mortgage & liquidity

I originate very few 15 year mortgages. The reason? I believe that cash is king. Given that mortgage rates are at historical low levels I would rather see my clients take out a 30 year amortizing mortgage and invest the difference instead of potentially creating a cash-trap with a 15 year loan. Here's an article that was published in the Wall Street Journal that places a 30-year mortgage at the top of the list for "surviving a cash crunch":

Take Seven Steps

So You Survive

A Cash Crunch

By BRETT ARENDS

April 12, 2008

No one wants to get caught in a cash crunch. Look at what happened to Bear Stearns.

Investors can't go running to the Fed.

Sometimes all it can take is a surprise bill, or a sudden loss of a job, to put your family's liquidity in peril. And these are treacherous times. The economy is rocky. Employers are cutting jobs. And some investments -- including home values -- are turning wobbly just when you may need them most.

The Federal Reserve, alas, isn't going to bail you out if you get hit by a liquidity crisis.

So where can you turn? If you're worried, check out your emergency lines of credit now, before there's a crisis.

Here are the seven habits of highly liquid people.

1. Refinance your mortgage over 30 years. Just switching your remaining debt from, say, a 20-year schedule will slash your monthly outflows by nearly a fifth. Borrowing against your home is the cheapest form of consumer debt.

2. Set up a home-equity line of credit. They're usually cheap to arrange, and you can draw on it when you need it. Right now, rates are as low as 5.25%.

3. Get a free float from a new credit card. Some still offer zero-percent interest on balances transferred from your current card. As always with the credit-card sharks: Watch out or they'll find a way to sock you with fees anyway.

4. Get your money back early from the IRS. Most Americans prepay too much tax, and the average refund is nearly $2,500. File a new W-4 with your employer to cut your monthly withholding. You have to estimate your likely bill in good faith. If you end up prepaying too little, you can make it up by Dec. 31. If you don't, you will have to pay 7% or so in penalties. The rate fluctuates, but it's a lot cheaper than an unsecured loan.

5. Set up unsecured financing sources now, while you don't need them. Ask your bank for an overdraft facility, of course. And apply for some emergency credit cards. Yes, the rates are usurious, so don't use them unless you have to. But someday you may have to.

6. Check out how to borrow from your 401(k) retirement plan. Most plans allow this, though the rules vary. The limits are often 50% of your balance, up to $50,000. It can take anywhere from a few days to a few weeks to get the money. Note: You may end up paying taxes, plus a 10% penalty, if you don't repay the money when you leave your employer, or within a specified period. It is usually five years. Check the rules ahead of time.

7. And, most obvious: Start saving. Most middle-class families can save thousands a year just by paring back on discretionary bills. This is a good time to slash those bills to the bone.

Take Seven Steps

So You Survive

A Cash Crunch

By BRETT ARENDS

April 12, 2008

No one wants to get caught in a cash crunch. Look at what happened to Bear Stearns.

Investors can't go running to the Fed.

Sometimes all it can take is a surprise bill, or a sudden loss of a job, to put your family's liquidity in peril. And these are treacherous times. The economy is rocky. Employers are cutting jobs. And some investments -- including home values -- are turning wobbly just when you may need them most.

The Federal Reserve, alas, isn't going to bail you out if you get hit by a liquidity crisis.

So where can you turn? If you're worried, check out your emergency lines of credit now, before there's a crisis.

Here are the seven habits of highly liquid people.

1. Refinance your mortgage over 30 years. Just switching your remaining debt from, say, a 20-year schedule will slash your monthly outflows by nearly a fifth. Borrowing against your home is the cheapest form of consumer debt.

2. Set up a home-equity line of credit. They're usually cheap to arrange, and you can draw on it when you need it. Right now, rates are as low as 5.25%.

3. Get a free float from a new credit card. Some still offer zero-percent interest on balances transferred from your current card. As always with the credit-card sharks: Watch out or they'll find a way to sock you with fees anyway.

4. Get your money back early from the IRS. Most Americans prepay too much tax, and the average refund is nearly $2,500. File a new W-4 with your employer to cut your monthly withholding. You have to estimate your likely bill in good faith. If you end up prepaying too little, you can make it up by Dec. 31. If you don't, you will have to pay 7% or so in penalties. The rate fluctuates, but it's a lot cheaper than an unsecured loan.

5. Set up unsecured financing sources now, while you don't need them. Ask your bank for an overdraft facility, of course. And apply for some emergency credit cards. Yes, the rates are usurious, so don't use them unless you have to. But someday you may have to.

6. Check out how to borrow from your 401(k) retirement plan. Most plans allow this, though the rules vary. The limits are often 50% of your balance, up to $50,000. It can take anywhere from a few days to a few weeks to get the money. Note: You may end up paying taxes, plus a 10% penalty, if you don't repay the money when you leave your employer, or within a specified period. It is usually five years. Check the rules ahead of time.

7. And, most obvious: Start saving. Most middle-class families can save thousands a year just by paring back on discretionary bills. This is a good time to slash those bills to the bone.

Financial Literacy article in the Economist

I've blogged before about how impressed I am with the coverage that the Economist Magazine has provided throughout the credit crunch that we currently find ourselves in. My praise continues this week. They have published an article pointing out the importance of teaching the masses about financial literacy. I have said all along that the subprime mortgage mess is the fault of many of the parties involved. However, the best way to fix the situation does not lie in government regulation. Instead, it lies in teaching people responsible money management skills which is something that is currently lacking in our education system. Hoooorah for the Economist!

Economist article:

Financial literacy

Getting it right on the money

Apr 3rd 2008 | NEW YORK

From The Economist print edition

A global crusade is under way to teach personal finance to the masses

“EVERYBODY wants it. Nobody understands it. Money is the great taboo. People just won't talk about it. And that is what leads you to subprime. Take the greed and the financial misrepresentation out of it, and the root of this crisis is massive levels of financial illiteracy.”

For years John Bryant has been telling anyone who will listen about the problems caused by widespread ignorance of finance. In 1992, in the aftermath of the Los Angeles riots, he founded Operation HOPE, a non-profit organisation, to give poor people in the worst-hit parts of the city “a hand-up, not a handout” through a mixture of financial education, advice and basic banking. Among other things, Operation HOPE offers mortgage advice to homebuyers and runs “Banking on Our Future”, a national personal-finance course of five hour-long sessions that has already been taken by hundreds of thousands of young people, most of them high-school students.

That many poor people do not have a bank account—and that few of them understand why this puts them at a disadvantage (let alone other essentials of personal finance)—is at the heart of “the civil-rights issue of the 21st century”, says Mr Bryant. He calls the attempt to help people help themselves out of poverty through financial literacy and economic opportunity the “silver-rights movement”.

In January George Bush appointed Mr Bryant vice-chairman of his new President's Council on Financial Literacy. This was launched as part of his administration's increasingly frenetic response to the financial crisis that followed the meltdown in subprime mortgages, many of them given to borrowers who may not have understood the risks. Often borrowers did not even realise that their monthly payment would rise if interest rates went up, says Mr Bryant. Subprime borrowers on adjustable interest rates, whose mortgages make up just 7% of the total, accounted for more than 40% of the foreclosures begun in the fourth quarter of last year.

The council is not short of expertise. It is chaired by Charles Schwab, eponymous boss of a broking firm. Its other members include the head of Junior Achievement, which has been teaching children about money since 1919, and a co-author of “Rich Dad, Poor Dad”, a self-help bestseller. Already, it has approved a new curriculum for middle-school students, “MoneyMath: Lessons for Life”. (Lesson one: the secret to becoming a millionaire. Answer: save, save, save.) It is starting a pilot programme to work out how to connect the “unbanked” to financial institutions. And it is supporting what, echoing the Peace Corps, is called the Financial Literacy Corps: a group of people with knowledge of finance who will volunteer to advise those in financial difficulties.

April has been declared Financial Literacy Month by Congress. The need to make this more than a slogan is especially apparent this year. But America is not the only country where doing something about the widespread ignorance of personal finance is on the agenda. Governments from Britain to Russia are declaring their commitment to financial education. This month the World Savings Banks Institute, which represents retail and savings banks from 92 countries, will hold a summit in Brussels about financial education in the light of the subprime crisis.

Meanwhile, on March 17th a new campaign to promote financial literacy in the developing world was launched at a conference in Amsterdam. Called Aflatoun (“Explorer”), after a cartoon character based on a Bollywood star, it is the brainchild of Jeroo Billimoria, a social entrepreneur who previously worked with street children in India. Among other things, she founded a successful emergency 24-hour telephone service, called Childline. She found that many of the children she helped were entrepreneurial (indeed, such spirits may have played a part in their decision to leave home) and became convinced that, given better education, they would have done well in life.

Ms Billimoria addresses herself to children aged between six and 14, whom most educators consider too young to understand money. Having begun with experiments in rural India, her non-profit organisation, Child Savings International, has piloted the Aflatoun course in 11 countries, including Argentina, South Africa, Vietnam and Zimbabwe, since 2005. It is now extending the course to 35 developing countries. Only recently, after suggestions from the Dutch central bank and the European Commission, has Ms Billimoria started to adapt Aflatoun for rich countries such as Britain, the Netherlands, Ireland and perhaps America. “My mistake. I never thought it would be needed in developed countries,” she says. If only.

Fools and their money

It is a “well-established fact” that “a substantial proportion of the general public in the English-speaking world is ignorant of finance,” writes Niall Ferguson, an historian at Harvard University, in his forthcoming book about the history of finance, “The Ascent of Money”. He produces a long list of evidence to support this conclusion. According to one survey last year, four in ten American credit-card holders do not pay the full amount due every month on the credit card they use most often, despite the punitive interest rates charged by credit-card companies. Nearly one-third said they had no idea what the interest rate on their credit card was.

There is similar evidence elsewhere. For instance, a survey in 2004 by Cambridge University and Prudential, a big insurer, found that some 9m Britons are “financially phobic”, meaning that “they shy away from anything to do with financial information, from bank statements to savings accounts to life assurance.” Research by the British regulator, the Financial Services Authority, found that one-quarter of adults did not realise that their pensions were invested in the stockmarket.

Financial illiteracy is not limited to subprime mortgage borrowers, then; it is pervasive in all age groups, income brackets and countries. “Subprime is a mere symptom,” says Mr Ferguson, noting that many of the students he has taught in the “best universities in the world, including MBA programmes, don't even know the difference between the nominal and real interest rate.” This problem is more pressing than ever, he adds, because governments and businesses have pushed more of the responsibility for financial well-being onto individuals, whether by encouraging homeownership or by promoting personally-managed retirement accounts rather than defined-benefit pensions.

The education system deserves much of the blame, says Mr Ferguson, who recalls having learnt nothing about personal finance at school in Scotland. In the 2007 survey of American credit-card holders, over half of the respondents said they had learnt “not too much” or “nothing at all” about finance at school.

Americans still leave school not knowing much about money. A sample of high-school pupils aged 17 or 18 gave correct answers to barely half of a set of questions about personal finance and economics posed in 2006 by researchers at the State University of New York, Buffalo. Less than one-quarter knew that income tax could be levied on interest earned in a savings account. Three-fifths did not know the difference between a company pension, Social Security and a 401(k) savings account.

The same survey, undertaken every two years for Jump$tart, a coalition of 180 organisations in America that promote financial literacy, found that one in six had taken part in a course dedicated to personal finance. A further one-third said they had learnt a bit from studying other subjects, such as business or economics. Laura Levine, the head of Jump$tart and a member of Mr Bush's financial-literacy council, says things are moving in the right direction, but that progress is slow. The results of the 2008 survey, which are unlikely to show much change, are due to be published on April 9th.

At present only three American states require that students take a course in personal finance. Another 15 insist that it be incorporated in other courses. Beyond that, it is a case of persuading schools one at a time. “Personal-finance education is not a hard sell conceptually,” says Ms Levine, “but only when it comes to getting it prioritised.” School principals will usually agree that financial literacy is worth teaching, but they are reluctant to give it time and resources.

Even when personal finance is taught, the right lessons are not necessarily learnt. “Wherever you look in America or the OECD, classes in financial literacy don't do much good,” says Lewis Mandell, an economist at Buffalo. “As an educator, I'd like to believe you can teach people to do anything right, but clearly the way we are going about teaching personal finance needs to be improved.”

To Mr Mandell's frustration, the only classroom method that seems consistently to raise financial literacy among high-school pupils is playing a stockmarket-investing game—which rewards taking high-risk bets. Most other approaches tend to show only short-term increases in financial literacy, he says.

According to Mr Mandell, one problem is that if financial literacy is taught, it tends to be before a student's final year—before she has faced any important financial decisions, such as buying a car or taking out a credit card. Another is that teachers are often financially illiterate, too. Financial literacy may be less about acquiring knowledge than forming good habits, something that is arguably better done before high school, let alone adulthood.

This is where Aflatoun comes in. Ms Billimoria encountered a great deal of scepticism when she developed her financial-literacy programme for six- to 14-year-olds. Yet she was convinced that starting with youngsters would be more effective, because that is “when their concept of themselves is developing and by 14 most of their habits have formed.”

An important part of the teaching is getting the children to start saving, ideally by opening bank accounts. Typically, they have only tiny amounts, but this is enough to get them used to handling money properly. At first this faced a lot of resistance, as people asked, “How can young children handle money?” recalls Ms Billimoria, but “it soon caught on and parents started giving children money to save.” To demonstrate its broad applicability, Aflatoun was piloted in economies beset by different difficulties. Zimbabwe, for example, was selected for its astronomical inflation rate. The course was adapted to encourage children to save by buying assets such as pencils, which, unlike the country's money, could be a store of value.

A nudge in the right direction

“The depressing truth is that financial literacy is impossible, at least for many of the big financial decisions all of us have to take,” says Richard Thaler, a behavioural economist at the University of Chicago. Aptly for someone who has built his career on the study of irrational financial behaviour, Mr Thaler admits that even he finds it hard to know the right thing to do. “If these things are perplexing to people with PhDs in economics, financial literacy is not the right road to go down.”

Instead, policymakers should “focus on making the world easier”, he argues in a new book, “Nudge: Improving Decisions About Health, Wealth and Happiness”, written with Cass Sunstein, a law professor (and an adviser to Barack Obama). By this he means defining more carefully and simply the financial choices that people have to make, and building “sensible default options” into the design of financial products, so that the do-nothing option is “financially literate”. Today, the best choice typically requires some working out and an active decision.

This does not mean that the same choice is right for everyone. The growing complexity of financial choices in part reflects remarkable innovation, much of which has benefited consumers. As Operation HOPE's Mr Bryant points out, thanks to the availability of subprime mortgages, “homeownership has lifted many poor people out of poverty; the challenge is to make the product better.”

Sweden's system of saving for old age contains an example of what Mr Thaler means. It offers Swedes a choice of funds to invest in, but includes a well-designed low-cost default option, which has become the choice of 90% of the people. The same approach might be taken to America's company 401(k) retirement plans, in which today's choices require a high degree of financial literacy. Employees might also be automatically enrolled in savings plans, with a right to opt out, instead of today's under-used opt-ins.

Mr Thaler deserves to be taken seriously, as one of his earlier attempts to apply behavioural economics to saving has had impressive results. Recognising that people find it harder to save money they already possess than to promise to put aside what they might have one day, he designed the Save More Tomorrow scheme, which gets people to commit themselves to saving a slice of any future pay increases. Where implemented, the plan has already brought about sharp increases in saving rates.

Another idea would make it easier for people to choose a suitable credit card, by obliging card companies to supply customers with two downloadable files, perhaps once a year. One would explain the issuer's charging rules; the other would list the charges the consumer has actually incurred. The consumer could then upload this to one of several websites that Mr Thaler believes would soon appear. With one click, the most suitable card would be recommended. A similar system could work for America's Medicare prescription programme, in which preliminary research suggests that matching the drugs a person needs with the right insurance plan would save on average $700 a year, he says.

Better product design and financial education need not be alternatives, points out Mr Mandell. They can work in tandem. He is enthusiastic about schemes such as the Child Trust Funds introduced in Britain. These “baby bonds” give every child a fund that matures at adulthood, letting everyone start out with a nest-egg. Mr Mandell is particularly excited by the curriculum being designed to be taught in conjunction with these funds, starting when children reach the age of seven. “Teachers will be able to talk about money realistically, because the kids will have ownership of wealth.”

If you can make it there

One of the most interesting attempts to combine teaching and superior products is taking place in New York, championed by a mayor, Michael Bloomberg, who made his fortune selling financial information. He has created an Office of Financial Empowerment, which is trying to use the powers of government to promote both financial education and better design of financial products.

The city's regulatory powers mean that it can crack down on firms that exploit financial literacy, and educate the public at the same time, says Jonathan Mintz, New York's Commissioner of Consumer Affairs. It has found that many tax-preparation agencies are offering “rapid refunds” which, as many consumers do not realise, are in fact loans in anticipation of refunds. Its publicity blitz about these loans led to coverage on news programmes “in 22 states and Canada”, allowing the city to promote the message that “anyone promising a tax refund within two days is selling a loan—don't do it.”

Another initiative is to use the city's system of helping people to apply for the earned income-tax credit as a chance to encourage them to open a bank account. As well as explaining to applicants the importance of saving, the city is working with banks to offer carefully designed accounts, and has even persuaded some philanthropists to provide matching funds for the first $250 someone saves. “You are not just educating me, you are allowing me to nod my head and say yes, and get a windfall,” says Mr Mintz. “Financial education is much more effective when it is connected to something real that is happening.”

With Miami, San Antonio, San Francisco, Savannah and Seattle, New York has formed the Cities for Financial Empowerment Coalition, which met for the first time to share ideas on March 18th. There was general agreement that education and better product design should go hand in hand. Most big banks have started to sponsor financial-literacy efforts, if only to cover their backs. However, Mr Mandell remarks, by increasing the charges for bank accounts with only small balances they have in effect deprived children of what was traditionally the best practical educational tool, an account of their own.

Indeed, one of the biggest problems may be the illiteracy of financial-service firms, which often fail to provide the products that poor consumers most want. That, at least, seems to be the conclusion of a recent survey in two of New York's poorer neighbourhoods. Many people were using fringe financial products such as pay-day loans or money orders rather than the services of mainstream banks.

The mainstream financial providers are “missing genuine markets”, says Mr Mintz. “One of the open secrets in this industry is that when people are engaged in behaviour that seems irrational, often it has a rational basis.” Which only goes to show that consumers are sometimes only as literate as the products the financial-services industry chooses to sell them.

Mr Bryant makes the same point more colourfully, noting that some of the first people to be hit by the subprime-mortgage crisis were the very brokers who had sold people inappropriate mortgages. Having drunk their own Kool-Aid, they found themselves with enormous debts and no job. “It takes less credentials to be a mortgage broker than a pimp on a street corner in Harlem,” he says. “Because a pimp needs references.”

Economist article:

Financial literacy

Getting it right on the money

Apr 3rd 2008 | NEW YORK

From The Economist print edition

A global crusade is under way to teach personal finance to the masses

“EVERYBODY wants it. Nobody understands it. Money is the great taboo. People just won't talk about it. And that is what leads you to subprime. Take the greed and the financial misrepresentation out of it, and the root of this crisis is massive levels of financial illiteracy.”

For years John Bryant has been telling anyone who will listen about the problems caused by widespread ignorance of finance. In 1992, in the aftermath of the Los Angeles riots, he founded Operation HOPE, a non-profit organisation, to give poor people in the worst-hit parts of the city “a hand-up, not a handout” through a mixture of financial education, advice and basic banking. Among other things, Operation HOPE offers mortgage advice to homebuyers and runs “Banking on Our Future”, a national personal-finance course of five hour-long sessions that has already been taken by hundreds of thousands of young people, most of them high-school students.

That many poor people do not have a bank account—and that few of them understand why this puts them at a disadvantage (let alone other essentials of personal finance)—is at the heart of “the civil-rights issue of the 21st century”, says Mr Bryant. He calls the attempt to help people help themselves out of poverty through financial literacy and economic opportunity the “silver-rights movement”.

In January George Bush appointed Mr Bryant vice-chairman of his new President's Council on Financial Literacy. This was launched as part of his administration's increasingly frenetic response to the financial crisis that followed the meltdown in subprime mortgages, many of them given to borrowers who may not have understood the risks. Often borrowers did not even realise that their monthly payment would rise if interest rates went up, says Mr Bryant. Subprime borrowers on adjustable interest rates, whose mortgages make up just 7% of the total, accounted for more than 40% of the foreclosures begun in the fourth quarter of last year.

The council is not short of expertise. It is chaired by Charles Schwab, eponymous boss of a broking firm. Its other members include the head of Junior Achievement, which has been teaching children about money since 1919, and a co-author of “Rich Dad, Poor Dad”, a self-help bestseller. Already, it has approved a new curriculum for middle-school students, “MoneyMath: Lessons for Life”. (Lesson one: the secret to becoming a millionaire. Answer: save, save, save.) It is starting a pilot programme to work out how to connect the “unbanked” to financial institutions. And it is supporting what, echoing the Peace Corps, is called the Financial Literacy Corps: a group of people with knowledge of finance who will volunteer to advise those in financial difficulties.

April has been declared Financial Literacy Month by Congress. The need to make this more than a slogan is especially apparent this year. But America is not the only country where doing something about the widespread ignorance of personal finance is on the agenda. Governments from Britain to Russia are declaring their commitment to financial education. This month the World Savings Banks Institute, which represents retail and savings banks from 92 countries, will hold a summit in Brussels about financial education in the light of the subprime crisis.

Meanwhile, on March 17th a new campaign to promote financial literacy in the developing world was launched at a conference in Amsterdam. Called Aflatoun (“Explorer”), after a cartoon character based on a Bollywood star, it is the brainchild of Jeroo Billimoria, a social entrepreneur who previously worked with street children in India. Among other things, she founded a successful emergency 24-hour telephone service, called Childline. She found that many of the children she helped were entrepreneurial (indeed, such spirits may have played a part in their decision to leave home) and became convinced that, given better education, they would have done well in life.

Ms Billimoria addresses herself to children aged between six and 14, whom most educators consider too young to understand money. Having begun with experiments in rural India, her non-profit organisation, Child Savings International, has piloted the Aflatoun course in 11 countries, including Argentina, South Africa, Vietnam and Zimbabwe, since 2005. It is now extending the course to 35 developing countries. Only recently, after suggestions from the Dutch central bank and the European Commission, has Ms Billimoria started to adapt Aflatoun for rich countries such as Britain, the Netherlands, Ireland and perhaps America. “My mistake. I never thought it would be needed in developed countries,” she says. If only.

Fools and their money

It is a “well-established fact” that “a substantial proportion of the general public in the English-speaking world is ignorant of finance,” writes Niall Ferguson, an historian at Harvard University, in his forthcoming book about the history of finance, “The Ascent of Money”. He produces a long list of evidence to support this conclusion. According to one survey last year, four in ten American credit-card holders do not pay the full amount due every month on the credit card they use most often, despite the punitive interest rates charged by credit-card companies. Nearly one-third said they had no idea what the interest rate on their credit card was.

There is similar evidence elsewhere. For instance, a survey in 2004 by Cambridge University and Prudential, a big insurer, found that some 9m Britons are “financially phobic”, meaning that “they shy away from anything to do with financial information, from bank statements to savings accounts to life assurance.” Research by the British regulator, the Financial Services Authority, found that one-quarter of adults did not realise that their pensions were invested in the stockmarket.

Financial illiteracy is not limited to subprime mortgage borrowers, then; it is pervasive in all age groups, income brackets and countries. “Subprime is a mere symptom,” says Mr Ferguson, noting that many of the students he has taught in the “best universities in the world, including MBA programmes, don't even know the difference between the nominal and real interest rate.” This problem is more pressing than ever, he adds, because governments and businesses have pushed more of the responsibility for financial well-being onto individuals, whether by encouraging homeownership or by promoting personally-managed retirement accounts rather than defined-benefit pensions.

The education system deserves much of the blame, says Mr Ferguson, who recalls having learnt nothing about personal finance at school in Scotland. In the 2007 survey of American credit-card holders, over half of the respondents said they had learnt “not too much” or “nothing at all” about finance at school.

Americans still leave school not knowing much about money. A sample of high-school pupils aged 17 or 18 gave correct answers to barely half of a set of questions about personal finance and economics posed in 2006 by researchers at the State University of New York, Buffalo. Less than one-quarter knew that income tax could be levied on interest earned in a savings account. Three-fifths did not know the difference between a company pension, Social Security and a 401(k) savings account.

The same survey, undertaken every two years for Jump$tart, a coalition of 180 organisations in America that promote financial literacy, found that one in six had taken part in a course dedicated to personal finance. A further one-third said they had learnt a bit from studying other subjects, such as business or economics. Laura Levine, the head of Jump$tart and a member of Mr Bush's financial-literacy council, says things are moving in the right direction, but that progress is slow. The results of the 2008 survey, which are unlikely to show much change, are due to be published on April 9th.

At present only three American states require that students take a course in personal finance. Another 15 insist that it be incorporated in other courses. Beyond that, it is a case of persuading schools one at a time. “Personal-finance education is not a hard sell conceptually,” says Ms Levine, “but only when it comes to getting it prioritised.” School principals will usually agree that financial literacy is worth teaching, but they are reluctant to give it time and resources.

Even when personal finance is taught, the right lessons are not necessarily learnt. “Wherever you look in America or the OECD, classes in financial literacy don't do much good,” says Lewis Mandell, an economist at Buffalo. “As an educator, I'd like to believe you can teach people to do anything right, but clearly the way we are going about teaching personal finance needs to be improved.”

To Mr Mandell's frustration, the only classroom method that seems consistently to raise financial literacy among high-school pupils is playing a stockmarket-investing game—which rewards taking high-risk bets. Most other approaches tend to show only short-term increases in financial literacy, he says.

According to Mr Mandell, one problem is that if financial literacy is taught, it tends to be before a student's final year—before she has faced any important financial decisions, such as buying a car or taking out a credit card. Another is that teachers are often financially illiterate, too. Financial literacy may be less about acquiring knowledge than forming good habits, something that is arguably better done before high school, let alone adulthood.

This is where Aflatoun comes in. Ms Billimoria encountered a great deal of scepticism when she developed her financial-literacy programme for six- to 14-year-olds. Yet she was convinced that starting with youngsters would be more effective, because that is “when their concept of themselves is developing and by 14 most of their habits have formed.”

An important part of the teaching is getting the children to start saving, ideally by opening bank accounts. Typically, they have only tiny amounts, but this is enough to get them used to handling money properly. At first this faced a lot of resistance, as people asked, “How can young children handle money?” recalls Ms Billimoria, but “it soon caught on and parents started giving children money to save.” To demonstrate its broad applicability, Aflatoun was piloted in economies beset by different difficulties. Zimbabwe, for example, was selected for its astronomical inflation rate. The course was adapted to encourage children to save by buying assets such as pencils, which, unlike the country's money, could be a store of value.

A nudge in the right direction

“The depressing truth is that financial literacy is impossible, at least for many of the big financial decisions all of us have to take,” says Richard Thaler, a behavioural economist at the University of Chicago. Aptly for someone who has built his career on the study of irrational financial behaviour, Mr Thaler admits that even he finds it hard to know the right thing to do. “If these things are perplexing to people with PhDs in economics, financial literacy is not the right road to go down.”

Instead, policymakers should “focus on making the world easier”, he argues in a new book, “Nudge: Improving Decisions About Health, Wealth and Happiness”, written with Cass Sunstein, a law professor (and an adviser to Barack Obama). By this he means defining more carefully and simply the financial choices that people have to make, and building “sensible default options” into the design of financial products, so that the do-nothing option is “financially literate”. Today, the best choice typically requires some working out and an active decision.

This does not mean that the same choice is right for everyone. The growing complexity of financial choices in part reflects remarkable innovation, much of which has benefited consumers. As Operation HOPE's Mr Bryant points out, thanks to the availability of subprime mortgages, “homeownership has lifted many poor people out of poverty; the challenge is to make the product better.”

Sweden's system of saving for old age contains an example of what Mr Thaler means. It offers Swedes a choice of funds to invest in, but includes a well-designed low-cost default option, which has become the choice of 90% of the people. The same approach might be taken to America's company 401(k) retirement plans, in which today's choices require a high degree of financial literacy. Employees might also be automatically enrolled in savings plans, with a right to opt out, instead of today's under-used opt-ins.

Mr Thaler deserves to be taken seriously, as one of his earlier attempts to apply behavioural economics to saving has had impressive results. Recognising that people find it harder to save money they already possess than to promise to put aside what they might have one day, he designed the Save More Tomorrow scheme, which gets people to commit themselves to saving a slice of any future pay increases. Where implemented, the plan has already brought about sharp increases in saving rates.

Another idea would make it easier for people to choose a suitable credit card, by obliging card companies to supply customers with two downloadable files, perhaps once a year. One would explain the issuer's charging rules; the other would list the charges the consumer has actually incurred. The consumer could then upload this to one of several websites that Mr Thaler believes would soon appear. With one click, the most suitable card would be recommended. A similar system could work for America's Medicare prescription programme, in which preliminary research suggests that matching the drugs a person needs with the right insurance plan would save on average $700 a year, he says.

Better product design and financial education need not be alternatives, points out Mr Mandell. They can work in tandem. He is enthusiastic about schemes such as the Child Trust Funds introduced in Britain. These “baby bonds” give every child a fund that matures at adulthood, letting everyone start out with a nest-egg. Mr Mandell is particularly excited by the curriculum being designed to be taught in conjunction with these funds, starting when children reach the age of seven. “Teachers will be able to talk about money realistically, because the kids will have ownership of wealth.”

If you can make it there

One of the most interesting attempts to combine teaching and superior products is taking place in New York, championed by a mayor, Michael Bloomberg, who made his fortune selling financial information. He has created an Office of Financial Empowerment, which is trying to use the powers of government to promote both financial education and better design of financial products.

The city's regulatory powers mean that it can crack down on firms that exploit financial literacy, and educate the public at the same time, says Jonathan Mintz, New York's Commissioner of Consumer Affairs. It has found that many tax-preparation agencies are offering “rapid refunds” which, as many consumers do not realise, are in fact loans in anticipation of refunds. Its publicity blitz about these loans led to coverage on news programmes “in 22 states and Canada”, allowing the city to promote the message that “anyone promising a tax refund within two days is selling a loan—don't do it.”

Another initiative is to use the city's system of helping people to apply for the earned income-tax credit as a chance to encourage them to open a bank account. As well as explaining to applicants the importance of saving, the city is working with banks to offer carefully designed accounts, and has even persuaded some philanthropists to provide matching funds for the first $250 someone saves. “You are not just educating me, you are allowing me to nod my head and say yes, and get a windfall,” says Mr Mintz. “Financial education is much more effective when it is connected to something real that is happening.”

With Miami, San Antonio, San Francisco, Savannah and Seattle, New York has formed the Cities for Financial Empowerment Coalition, which met for the first time to share ideas on March 18th. There was general agreement that education and better product design should go hand in hand. Most big banks have started to sponsor financial-literacy efforts, if only to cover their backs. However, Mr Mandell remarks, by increasing the charges for bank accounts with only small balances they have in effect deprived children of what was traditionally the best practical educational tool, an account of their own.

Indeed, one of the biggest problems may be the illiteracy of financial-service firms, which often fail to provide the products that poor consumers most want. That, at least, seems to be the conclusion of a recent survey in two of New York's poorer neighbourhoods. Many people were using fringe financial products such as pay-day loans or money orders rather than the services of mainstream banks.

The mainstream financial providers are “missing genuine markets”, says Mr Mintz. “One of the open secrets in this industry is that when people are engaged in behaviour that seems irrational, often it has a rational basis.” Which only goes to show that consumers are sometimes only as literate as the products the financial-services industry chooses to sell them.

Mr Bryant makes the same point more colourfully, noting that some of the first people to be hit by the subprime-mortgage crisis were the very brokers who had sold people inappropriate mortgages. Having drunk their own Kool-Aid, they found themselves with enormous debts and no job. “It takes less credentials to be a mortgage broker than a pimp on a street corner in Harlem,” he says. “Because a pimp needs references.”

Friday, April 11, 2008

Rate Update April 11, 2008

Mortgage rates increases yesterday afternoon by .125% but have since reversed back to the levels reported yesterday in ‘rate update’.

The bond market is trading slightly higher in response a weak stock market. The Dow Jones Industrial is currently down over 100 points in part because GE reported weak earnings and gave weak profit guidance.

We’ve talked about it before in ‘rate update’ but I have given an explanation as to why a weak stock market typically helps interest rates………

Current Outlook: neutral

Thursday, April 10, 2008

How am I compensated as a mortgage broker?

Our compensation typically ranges from 1-2% of the loan amount depending on the interest rate environment and type of loan we're providing.

With a 0% point loan structure the lender that we assign the servicing rights of your loan to will compensate us by paying us a fee for the right to collect the future mortgage payments. In this instance our client is not paying us our fee for originating the loan because the lender is.

Choosing a loan option with points is a little bit different. In this instance the borrower is paying us a fee of 0-2% that is paid at closing and is included in the closing costs. It is also possible that our compensation is paid as a combination between points charged to the borrower and fees collected from our lender. We are always happy to be transparent about our compensation so please feel free to ask us questions.

Our firm also charges a processing fee of $395 that will go towards the in-house processing of your mortgage paperwork. This insures that your loan closing will happen in a timely manner. If, for any reason your loan closes late because of an issue within our control we will absolutely refund this processing fee.

With a 0% point loan structure the lender that we assign the servicing rights of your loan to will compensate us by paying us a fee for the right to collect the future mortgage payments. In this instance our client is not paying us our fee for originating the loan because the lender is.

Choosing a loan option with points is a little bit different. In this instance the borrower is paying us a fee of 0-2% that is paid at closing and is included in the closing costs. It is also possible that our compensation is paid as a combination between points charged to the borrower and fees collected from our lender. We are always happy to be transparent about our compensation so please feel free to ask us questions.

Our firm also charges a processing fee of $395 that will go towards the in-house processing of your mortgage paperwork. This insures that your loan closing will happen in a timely manner. If, for any reason your loan closes late because of an issue within our control we will absolutely refund this processing fee.

What is a point?